Titan Company: The Business Behind India’s Obsession With Gold

Every Indian family owns gold.

Very few own the business that sells it.

For centuries, Indian households trusted local jewellers for one of life’s most emotional purchases. Weddings, festivals, anniversaries, and family milestones were all linked to neighbourhood jewellery stores built on personal relationships and reputation.

Titan changed that equation.

Through Tanishq, the company transformed trust into a scalable business model. It brought transparency, purity certification, design innovation, and modern retail practices to an industry that was historically fragmented and largely unorganized.

The result?

What started as a watch company became India’s largest organized jewellery retailer and one of the country’s most successful consumer franchises.

Today, Titan is no longer merely selling jewellery.

It is selling trust.

It is selling aspiration.

It is selling one of the most powerful consumer brands in India.

Yet investors face a difficult question.

At a market capitalization exceeding ₹3.6 lakh crore and a valuation near 70 times earnings, has the market already priced in years of future growth? Or does Titan still possess enough competitive advantage to justify its premium valuation?

This article applies Equity Blueprint’s 5-Layer Framework to answer that question.

Titan Investment Thesis in 30 Seconds

The Bull Case

✔ Industry leader in India’s organized jewellery market

✔ Massive beneficiary of the shift from unorganized to organized retail

✔ Strong portfolio of brands including Tanishq, Mia, Zoya, CaratLane, Titan Watches, Helios and Titan Eye+

✔ Exceptional capital efficiency with ROE above 37%

✔ Long runway through international expansion and premiumization

✔ Strong management execution over multiple economic cycles

The Bear Case

✖ Premium valuation of nearly 70x earnings

✖ Gold price volatility can impact demand

✖ Increasing competition from Kalyan, Senco and regional players

✖ High expectations leave little room for execution mistakes

✖ Working-capital-intensive business model

✖ International expansion introduces execution risk

Equity Blueprint Preliminary Verdict

Business Quality: Exceptional

Valuation Comfort: Limited

Investor Type: Long-term compounder-focused investors

Initial View: High-Quality Business, Premiumly Priced Stock

Quick Snapshot

| Metric | Titan Company | What It Means |

| Current Price | ₹4,105 | Premium valuation reflects strong market confidence |

| Market Capitalization | ₹3,64,501 Cr | One of India’s largest consumer companies |

| P/E Ratio | 73.5 | Expensive relative to most companies |

| 10-Year Median P/E | 80.6 | Trading below its own historical valuation average |

| Industry P/E | 16.4 | Titan commands a huge premium |

| PEG Ratio | 4.28 | Investors are paying heavily for growth |

| Debt-to-Equity | 0.93 | Elevated but expected for jewellery retail |

| ROE | 37.7% | Exceptional shareholder value creation |

| ROCE | 25.8% | High capital efficiency |

| Current Ratio | 1.28 | Adequate short-term liquidity |

| Quick Ratio | 0.20 | Inventory-heavy business model |

| Free Cash Flow (3 Years) | ₹4,726 Cr | Healthy cash generation capability |

| Revenue FY2015 | ₹11,913 Cr | Starting point of the growth journey |

| Revenue FY2026 | ₹87,584 Cr | More than 7x growth in 11 years |

| Profit FY2015 | ₹1,153 Cr | Base-year profitability |

| Profit FY2026 | ₹8,355 Cr | More than 7x profit growth |

Key Insight

Titan is not being valued as a jewellery retailer.

The market is valuing Titan as a long-duration consumer franchise capable of compounding earnings for decades.

Industry Landscape

Industry Overview

India’s jewellery industry occupies a unique position in the economy.

Unlike many consumer categories that depend purely on discretionary spending, jewellery combines consumption, culture, savings, investment, and wealth preservation.

Gold jewellery in India is simultaneously:

- A luxury product

- A cultural necessity

- A savings instrument

- An inflation hedge

- A store of value

This makes the industry fundamentally different from most retail segments.

The Indian gems and jewellery industry is estimated to exceed $85 billion and remains one of the largest consumer sectors in the country.

Major segments include:

- Gold Jewellery

- Diamond Jewellery

- Bridal Jewellery

- Luxury Jewellery

- Fashion Jewellery

- Silver Jewellery

- Digital Jewellery Retail

While industry growth can fluctuate with economic conditions and gold prices, long-term demand remains supported by demographics, rising incomes, and cultural preferences.

Why This Industry Matters

Many industries require consumers to spend more.

Jewellery often benefits simply because consumers continue saving.

In India, gold remains one of the most trusted financial assets across generations. That creates a structural demand foundation that few industries enjoy.

Industry Value Chain

Understanding the value chain helps investors identify where profits are created.

The jewellery industry typically follows this structure:

Mining & Refining → Bullion Importers → Manufacturers → Designers → Retailers → Consumers

Historically, most participants competed largely on product availability and local relationships.

Today’s organized market is different.

The highest-value participants increasingly compete through:

- Brand trust

- Product design

- Customer experience

- Store network

- Digital engagement

- Loyalty programs

- Omnichannel retailing

Titan operates at the most profitable end of the value chain.

The company does not merely sell gold.

It monetizes trust.

This distinction is extremely important because trust creates pricing power.

Pricing power creates superior returns on capital.

Superior returns on capital create long-term shareholder wealth.

The Titan Advantage

Local jewellers sell jewellery.

Titan sells jewellery plus trust.

That difference explains why Titan earns premium valuations while much of the industry does not.

Key Industry Growth Drivers

1. Formalization of the Jewellery Industry

The biggest structural trend in Indian jewellery is the migration from unorganized players toward branded retailers.

Several factors are accelerating this shift:

- GST implementation

- Mandatory hallmarking

- Greater transparency

- Consumer awareness

- Digital influence

Every year, a small percentage of customers move from local jewellers to organized brands.

Titan remains one of the largest beneficiaries of this migration.

2. Rising Disposable Income

India’s expanding middle class continues to increase spending on premium products.

As incomes rise, consumers often upgrade from local jewellery stores to trusted national brands.

This premiumization trend directly supports Titan’s growth.

3. Wedding Economy

India’s wedding industry remains one of the largest globally.

Jewellery represents a major portion of wedding expenditure.

Even during economic slowdowns, wedding-related jewellery demand often remains resilient. This provides a natural support system for industry growth.

4. Digital and Omnichannel Retail

Consumers increasingly discover products online before purchasing offline.

Titan has invested heavily in omnichannel capabilities through Tanishq and CaratLane.

This allows the company to capture digitally influenced demand more effectively than traditional competitors.

5. International Expansion

The global Indian diaspora creates a natural market for branded Indian jewellery.

Titan has expanded aggressively into:

- UAE

- GCC Region

- United States

- Singapore

International expansion remains one of the largest growth opportunities over the next decade.

Industry Risks

No industry is risk-free.

Investors must understand both cyclical and structural challenges.

Gold Price Volatility

Rapid increases in gold prices can reduce affordability and temporarily impact consumer demand.

Although revenues may increase because of higher realizations, volume growth can slow.

Regulatory Risk

Import duties, hallmarking regulations, taxation policies and compliance requirements can materially affect profitability.

Titan experienced this firsthand when customs duty changes impacted inventory economics during FY25.

Working Capital Intensity

Jewellery retail requires large inventory holdings.

Significant capital remains tied up in gold inventory.

Efficient inventory management becomes a major competitive advantage.

Competitive Pressure

The industry remains highly fragmented.

Organized competitors continue expanding aggressively.

Key competitors include:

- Kalyan Jewellers

- Senco Gold

- Thangamayil Jewellery

- PC Jeweller

- Numerous regional players

Economic Slowdowns

Premium jewellery purchases can be affected by weaker consumer sentiment.

Although wedding demand remains relatively resilient, discretionary spending may slow during economic stress.

Industry Structure

The Indian jewellery market remains one of the most fragmented large industries in the country.

Even today, the majority of market share remains outside the organized sector.

This is important because it creates a long-term growth runway for large branded players.

Unlike industries that have already matured, jewellery still offers significant market-share opportunities.

Titan’s future growth does not require dramatic industry expansion.

It only requires continued migration toward organized retail.

Industry Outlook (2026–2030)

The next three to five years appear structurally favorable.

Major opportunities include:

- Formalization

- Premiumization

- Rising household incomes

- Expansion into Tier-2 and Tier-3 cities

- International growth

- Digital commerce

Major risks include:

- Sustained gold-price inflation

- Regulatory intervention

- Economic slowdown

- Margin pressure from competition

Overall, the long-term outlook remains positive.

The central investment question is no longer whether the jewellery industry will grow.

The real question is:

Can Titan continue growing faster than the industry while maintaining premium profitability?

That is what we will evaluate in Layer 1 of the Equity Blueprint framework.

Industry Positioning: Where Does Titan Stand?

Titan is not a turnaround story.

It is not a niche player.

It is not a cyclical bet.

Titan is the undisputed leader of India’s organized jewellery industry.

Its competitive advantages include:

- Brand Trust

- Scale

- Distribution

- Design Capability

- Customer Loyalty

- Omnichannel Reach

- International Presence

The company increasingly resembles a consumer franchise rather than a traditional retailer.

And that distinction is exactly why investors are willing to pay premium valuations.

The next question is whether those valuations are justified.

Let’s examine the numbers.

Layer 1: Is Titan’s 70x P/E a Valuation Trap or a Quality Premium?

Every investor eventually faces a difficult question.

How much should you pay for quality?

The market rarely gives exceptional businesses away at cheap valuations. The best companies often appear expensive because investors are willing to pay for predictability, competitive advantages, and long growth runways.

Titan is a textbook example.

At approximately 70.8 times earnings, Titan is among the most expensive large-cap consumer companies in India. For value investors, that number alone may be enough to reject the stock immediately.

But valuation analysis requires context.

A 70x multiple can be dangerous for a mediocre business.

The same multiple may be justified for a dominant franchise capable of compounding earnings for decades.

The real question is not whether Titan is expensive.

The real question is whether Titan deserves to be expensive.

Let’s examine the evidence.

Titan vs Competitors: The Valuation Gap

The easiest way to understand Titan’s valuation is to compare it with other listed jewellery players.

Peer Comparison

| Company | P/E | PEG | Debt/Equity | ROE | ROCE |

| Titan Company | 73.5 | 4.44 | 0.93 | 37.7% | 25.8% |

| Kalyan Jewellers | 27.9 | 0.63 | 0.97 | 24.8% | 20.5% |

| Thangamayil Jewellery | 47.1 | 0.73 | 0.64 | 28.1% | 25.5% |

| Senco Gold | 9.87 | 0.18 | 1.07 | 25.6% | 20.9% |

| PC Jeweller | 12.5 | 0.16 | 0.14 | 9.96% | 9.58% |

At first glance, Titan appears outrageously expensive.

Its valuation is:

- Nearly 7 times Senco Gold

- More than 5 times PC Jeweller

- Almost 3 times Kalyan Jewellers

If valuation were the only consideration, Titan would look unattractive.

But markets rarely reward companies solely for current earnings.

They reward expected future earnings.

And that is where Titan begins to separate itself.

Why Does Titan Trade at Such a Premium?

The market is paying for five factors.

1. Industry Leadership

Titan is not merely another jewellery retailer.

It is the category leader.

Leadership matters because leaders typically capture disproportionate benefits when industries formalize.

As local jewellers gradually lose share, Titan becomes one of the primary destinations for migrating customers.

2. Trust as a Competitive Advantage

Most businesses compete on price.

Titan competes on trust.

When consumers purchase jewellery worth several lakhs of rupees, trust becomes a critical decision factor.

Trust is difficult to measure.

But it is extremely valuable.

The market recognizes this.

3. Brand Portfolio

Most competitors rely heavily on a single brand.

Titan operates multiple growth engines:

- Tanishq

- Mia

- Zoya

- CaratLane

- Titan Watches

- Helios

- Titan Eye+

- SKINN

- Taneira

This diversification reduces business risk.

4. Capital Efficiency

The market rewards companies that generate high returns on capital.

Titan’s:

- ROE = 37.7%

- ROCE = 25.8%

These numbers place Titan among the elite capital allocators in Indian consumer markets.

5. Growth Visibility

Investors have greater confidence in Titan’s future earnings trajectory than most competitors.

The market believes:

- Industry formalization will continue.

- Market-share gains will continue.

- Premiumization will continue.

- International expansion will continue.

Whether these assumptions prove correct remains to be seen.

But current valuations clearly reflect those expectations.

Market Psychology

Investors are not paying 70x earnings for Titan’s current profits.

They are paying for what Titan’s profits might look like ten years from now.

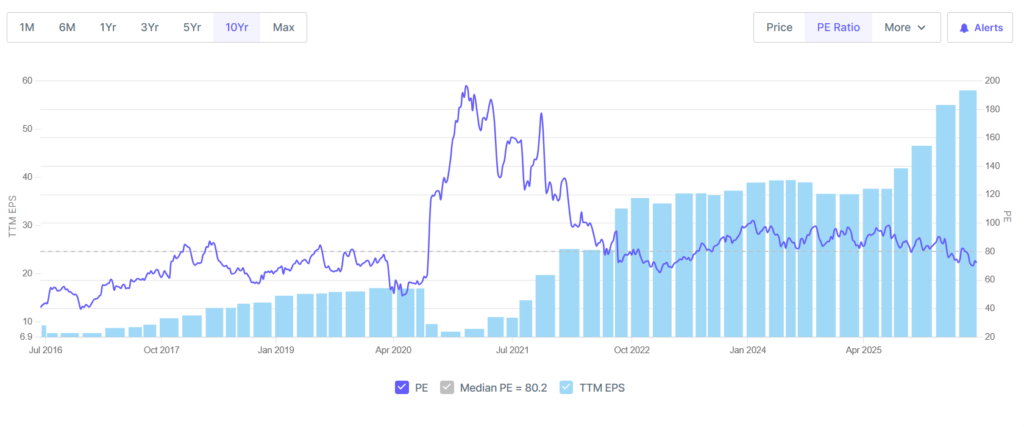

Is Titan Actually Cheap Relative to Its Own History?

Image Source: https://www.screener.in/

This is where things become interesting.

Most investors compare Titan only with competitors.

A more useful comparison is Titan versus Titan.

Historical P/E Context

Current P/E: 70.8

10-Year Median P/E: 80.6

That means Titan is actually trading below its own long-term valuation average.

This does not automatically make the stock cheap.

But it does challenge the narrative that Titan is trading at unprecedented valuations.

Historically, the market has consistently assigned premium multiples to Titan because it has consistently delivered premium execution.

The stock has rarely been available at traditional value-investing valuations.

Investors waiting for Titan to trade at 15x earnings have been waiting for decades.

The PEG Ratio Problem

While the P/E argument can be defended, the PEG ratio deserves greater scrutiny.

Titan’s PEG ratio stands at approximately 4.28.

For context:

- PEG below 1 often suggests attractive valuation relative to growth.

- PEG around 1–2 is generally considered reasonable.

- PEG above 3 usually signals aggressive expectations.

Titan’s PEG ratio indicates investors are paying a substantial premium for future growth.

This creates an important implication.

Even if the company continues growing strongly, shareholder returns may disappoint if growth falls short of expectations.

The stock no longer requires good execution. It requires excellent execution.

Debt Analysis: Should Investors Worry?

Many investors see Titan’s Debt-to-Equity ratio of 0.93 and immediately become concerned.

That reaction is understandable.

But context matters.

Jewellery retail is fundamentally different from software businesses or asset-light consumer companies.

Gold inventory must be financed.

As gold prices rise, inventory values increase.

This naturally increases financing requirements.

Therefore, debt should not be analyzed in isolation.

It should be analyzed alongside:

- Inventory economics

- Return on capital

- Cash generation

- Market position

Viewed through this lens, Titan’s debt appears manageable.

The company continues generating:

- Strong ROE

- Strong ROCE

- Positive free cash flow

- Robust profitability

These characteristics suggest that debt remains a tool supporting growth rather than a sign of financial stress.

Liquidity Analysis: The Quick Ratio Looks Scary… But Isn’t

One number often alarms inexperienced investors.

Titan’s Quick Ratio: 0.20

At first glance, that looks terrible.

Most textbooks suggest higher liquidity ratios.

However, jewellery retail requires large inventory holdings.

Most of Titan’s capital is effectively sitting inside gold inventory.

This creates a structurally low quick ratio.

The key question is not:

“Why is the quick ratio low?”

The key question is:

“Can Titan efficiently convert inventory into sales and profits?”

History suggests the answer is yes.

Why This Matters

A low quick ratio is dangerous when inventory cannot be sold.

Titan’s inventory is gold.

Gold is among the most liquid assets in the world.

That changes the risk profile significantly.

The Hidden Valuation Risk Nobody Talks About

Most investors focus on business risk.

The larger risk today may actually be valuation risk.

Consider two scenarios.

Scenario A

Titan grows earnings at 18–20% annually for several years.

Valuation remains stable.

Investors earn attractive returns.

Scenario B

Titan grows earnings at 18–20% annually.

But valuation falls from 70x earnings to 45x earnings.

Business performance remains excellent.

Stock returns become significantly lower.

This is why investing in premium companies requires discipline.

The quality of the business does not guarantee the attractiveness of the stock.

The entry price still matters.

Equity Blueprint Assessment: Layer 1

After analyzing valuation, debt, liquidity, peer positioning, and market expectations, the conclusions are relatively straightforward.

Positives

✔ Industry-leading franchise

✔ Exceptional ROE and ROCE

✔ Strong growth visibility

✔ Premium brands

✔ Strong competitive moat

✔ Trading below its own historical valuation average

Concerns

✖ Expensive relative to peers

✖ PEG ratio indicates high expectations

✖ Limited margin of safety

✖ Valuation compression risk

Layer 1 Verdict

Titan is not a value stock.

Titan is not a bargain stock.

Titan is not a deep-discount opportunity.

Titan is a premium-quality compounder trading at a premium valuation.

Investors buying Titan today are effectively making a wager that the company will continue executing at an elite level for many years.

That may prove correct.

But the stock leaves little room for mistakes.

The next question is arguably even more important.

A premium valuation can only be justified if growth remains exceptional.

Has Titan actually delivered that growth over the past decade?

And more importantly, can it continue?

Layer 2: Growth Consistency — How Titan Turned ₹11,913 Crore Revenue Into ₹87,584 Crore Without Breaking the Business Model

Most companies can produce one great year.

Some companies can produce a great five-year period.

Very few companies can sustain growth through multiple economic cycles, regulatory shocks, commodity volatility, changing consumer behavior, and technological disruption.

This is where Titan begins to separate itself from most listed businesses.

The company’s biggest achievement is not its size.

Its biggest achievement is consistency.

Over the last decade, Titan has repeatedly demonstrated an ability to grow through both favorable and unfavorable environments.

That consistency is one of the primary reasons investors continue assigning premium valuations to the stock.

The market is not paying for what Titan achieved.

The market is paying for confidence that Titan can continue achieving it. Let’s examine whether that confidence is justified.

The Numbers Tell a Powerful Story

Revenue Growth

| Financial Year | Revenue |

| FY2015 | ₹11,913 Cr |

| FY2026 | ₹87,584 Cr |

Revenue increased more than 7 times over eleven years.

Profit Growth

| Financial Year | Net Profit |

| FY2015 | ₹1,153 Cr |

| FY2026 | ₹8,355 Cr |

Profit also increased more than 7 times during the same period.

Why These Numbers Matter

Revenue growth alone means very little.

Many companies can grow revenue by sacrificing margins.

Profit growth alone can also be misleading because temporary cost reductions can inflate earnings.

Titan achieved both simultaneously.

Revenue expanded dramatically.

Profit expanded proportionately.

This indicates that growth was supported by genuine business strength rather than accounting adjustments or financial engineering.

The Big Picture

Titan did not merely become bigger.

Titan became bigger while maintaining attractive profitability. That distinction separates compounders from pretenders.

The Growth Journey Was Not Smooth

Looking only at the final numbers creates a dangerous illusion.

It makes Titan’s growth appear easy.

It wasn’t.

The company navigated some of the most disruptive events in modern Indian retail history.

Demonetization

In 2016, demonetization disrupted consumer spending across multiple sectors.

Jewellery retailers experienced significant uncertainty.

Titan survived.

GST Implementation

GST transformed the economics of the jewellery industry.

Many smaller players struggled to adapt.

Titan gained share.

COVID-19

This was arguably the largest stress test.

Retail stores closed.

Consumer mobility collapsed.

Supply chains were disrupted.

Yet Titan emerged stronger.

Gold Price Volatility

Gold prices experienced multiple periods of extreme volatility.

Consumer behavior changed.

Product mix shifted.

Demand patterns evolved.

Titan adapted.

Customs Duty Changes

FY25 provided another example.

Changes in import duties created inventory-related profitability pressure.

Management openly acknowledged the impact.

The business continued growing.

Why Titan Keeps Winning During Disruptions

The answer lies in market structure.

Most industries become harder during disruptions.

Titan’s industry often becomes easier.

That may sound strange.

But consider what happens during periods of uncertainty.

Consumers become more cautious.

Trust becomes more important.

Purchases become more selective.

This environment often hurts smaller players more than larger brands.

When consumers become uncertain about purity, pricing, transparency, or quality, they gravitate toward trusted names.

Titan benefits from this behavior.

Every major disruption over the last decade has accelerated industry formalization.

And industry formalization is one of Titan’s most powerful growth drivers.

The Structural Growth Engine

The most important question investors should ask is:

Where is Titan’s growth actually coming from?

The answer is not simply “more jewellery sales.”

Titan’s growth comes from multiple structural drivers operating simultaneously.

Driver 1: Industry Formalization

The Indian jewellery market remains highly fragmented.

A large portion still belongs to local and regional players.

Every year, some consumers migrate toward organized retailers.

Titan captures a significant share of that migration. This creates a powerful structural tailwind.

Driver 2: Premiumization

Consumers increasingly prefer:

- Better designs

- Better retail experiences

- Certified purity

- Trusted brands

Premiumization allows Titan to grow faster than the underlying industry.

Driver 3: Store Expansion

Titan continues expanding across:

- Tanishq

- Mia

- Zoya

- CaratLane

- Titan Watches

- Helios

- Titan Eye+

- International markets

Each new store increases customer reach.

Each new customer strengthens the brand.

Driver 4: Category Expansion

Most investors think of Titan as a jewellery company.

Management thinks differently.

Over time, Titan has built multiple growth engines.

Examples include:

- Watches

- Premium Watches

- EyeCare

- Fragrances

- Fashion Accessories

- Women’s Bags

- Ethnic Wear

- International Retail

Some remain small today.

But they diversify future growth.

Driver 5: International Expansion

International revenue remains a relatively small portion of Titan’s overall business.

That is precisely why it is interesting.

Markets such as:

- UAE

- GCC Region

- United States

- Singapore

provide additional growth opportunities beyond India.

The Damas acquisition significantly strengthens this opportunity.

The Titan Growth Flywheel

One of the most powerful aspects of Titan’s business model is the self-reinforcing growth loop it has built over decades.

The Titan Flywheel

More Stores

↓

Higher Customer Reach

↓

Greater Brand Trust

↓

Premium Pricing Power

↓

Higher Cash Generation

↓

More Expansion Capital

↓

More Stores

The cycle repeats.

This is extremely difficult for smaller competitors to replicate.

Because the flywheel is already spinning.

Titan simply needs to keep it moving.

Revenue Growth Is No Longer Only About Jewellery

A common misconception is that Titan’s future depends entirely on Tanishq.

That was true a decade ago.

It is becoming less true every year.

Let’s examine some recent examples.

Watches Are Quietly Becoming a Major Growth Engine

The watches division has delivered some of its strongest performances in recent years.

Recent quarterly results showed:

- Double-digit growth

- Premiumization gains

- Strong Helios performance

- Robust analog watch demand

Interestingly, analog watches continue outperforming smartwatches in Titan’s portfolio. This suggests that Titan’s core strength remains branding rather than technology.

CaratLane Is Becoming Strategically Important

CaratLane is more than a subsidiary.

It is Titan’s bridge to younger consumers.

The brand continues delivering:

- Strong customer acquisition

- Digital engagement

- Store expansion

- Premium growth

This gives Titan exposure to demographics that may not initially enter through Tanishq.

EyeCare Has Returned to Growth

After periods of slower expansion, EyeCare has returned to double-digit growth.

Although still much smaller than jewellery, it contributes to diversification.

Emerging Businesses Continue Building Optionality

Fragrances.

Women’s Bags.

Taneira.

These businesses remain relatively small.

But together they create optionality.

Not every initiative will succeed.

The important point is that Titan is building future growth engines before it desperately needs them.

What Management Gets Right About Growth

Titan’s leadership has historically focused on quality growth.

The difference is critical.

Poor-quality growth often relies on:

- Aggressive discounting

- Excessive leverage

- Poor capital allocation

Titan’s growth has largely been supported by:

- Brand strength

- Market-share gains

- Store productivity

- Premiumization

- Customer trust

This is a much healthier foundation.

Why This Matters

Growth funded by debt eventually stops.

Growth funded by competitive advantage can continue for decades.

Titan’s growth has historically been driven by competitive advantage.

Can Titan Continue Growing?

This is the question that ultimately matters.

No company can grow at 40–50% forever.

The larger a business becomes, the harder growth becomes.

Titan now operates from a very large base.

Future growth rates will inevitably moderate.

However, moderation does not necessarily mean stagnation.

Several long-term opportunities remain:

- Industry formalization

- Premiumization

- International expansion

- CaratLane scaling

- Damas integration

- Emerging businesses

- Tier-2 and Tier-3 city penetration

Together, these drivers suggest that Titan still possesses a meaningful growth runway.

The company’s future may not look identical to its past.

But the structural foundations supporting growth remain intact.

Equity Blueprint Assessment: Layer 2

Positives

✔ Revenue increased from ₹11,913 Cr to ₹87,584 Cr

✔ Profit increased from ₹1,153 Cr to ₹8,355 Cr

✔ Growth survived multiple economic shocks

✔ Market-share gains continue

✔ Multiple growth engines beyond jewellery

✔ International expansion adds runway

Concerns

✖ Growth rates will naturally slow from a larger base

✖ Jewellery remains the dominant earnings contributor

✖ International expansion still carries execution risk

✖ Emerging businesses remain relatively small

Layer 2 Verdict

Titan’s growth appears overwhelmingly structural rather than cyclical.

The company is not merely benefiting from favorable economic conditions.

It is benefiting from long-term industry transformation.

That distinction matters because structural growth tends to persist longer than cyclical growth.

The evidence suggests Titan has earned its reputation as one of India’s premier long-term compounders.

However, sustained growth alone is not enough.

Investors must determine whether management deserves credit for this performance—or whether favorable industry conditions deserve most of the praise. That brings us to Layer 3.

Layer 3: Management Execution — Does Titan’s Leadership Deserve Investor Trust?

Investing ultimately comes down to one simple question.

Who is allocating your capital?

Financial statements tell investors what happened.

Management behavior helps investors understand what may happen next.

This distinction is important.

Many companies can produce impressive quarterly numbers.

Far fewer can consistently make intelligent decisions over decades.

The best management teams build institutions.

The average ones simply manage businesses.

Titan’s investment case becomes significantly stronger when viewed through this lens.

Over the last decade, management has navigated:

- Demonetization

- GST implementation

- COVID-19

- Gold-price volatility

- Customs duty changes

- International expansion

- Digital disruption

- Leadership transition

Yet the company emerged stronger after nearly every challenge.

That track record deserves attention.

The question is whether this success reflects exceptional management or simply favorable industry dynamics.

Let’s examine the evidence.

Management’s Most Important Achievement Is Not Revenue Growth

Most investors focus on revenue.

Some focus on profit.

The most impressive achievement may actually be something else.

Titan successfully institutionalized trust.

This sounds abstract.

But it is the foundation of the entire business.

Historically, jewellery purchases were trust-based transactions conducted through local relationships.

Customers trusted individual jewellers.

Titan transformed that model.

Customers now trust a brand.

That shift may be one of the most significant value-creation stories in Indian retail history.

Importantly, management did not achieve this through advertising alone.

They achieved it through decades of execution.

Trust cannot be purchased.

It must be earned.

A Decade of Capital Allocation Decisions

The quality of management becomes visible through capital allocation.

Let’s review some major strategic decisions.

Decision 1: Double Down on Tanishq

This may seem obvious today.

It wasn’t always.

Building a national jewellery brand required:

- Large inventory investments

- Store expansion

- Brand building

- Customer education

Management continued investing even when organized jewellery retail was still developing.

That decision created enormous shareholder value.

Decision 2: Create Multiple Brands

Many companies become dependent on one brand.

Titan deliberately built a portfolio.

Tanishq

Mass-premium jewellery.

Mia

Young urban women.

Zoya

Luxury jewellery.

CaratLane

Digital-first and younger consumers.

This segmentation reduces concentration risk.

It also expands Titan’s addressable market.

Decision 3: Build a Watch Ecosystem

Instead of relying solely on Titan Watches, management expanded into:

- Titan Premium

- Helios

- International Brands

- Fastrack

- Sonata

This broadened the business beyond traditional watch retail.

The result is a segment that continues generating healthy profits decades after inception.

Decision 4: Enter Emerging Categories

Not every initiative has succeeded.

But management consistently invested in optionality.

Examples include:

- Titan Eye+

- SKINN

- Taneira

- IRTH

These businesses remain relatively small.

However, they create future growth opportunities.

The willingness to experiment is important.

The discipline to avoid overcommitting is equally important. Titan has generally demonstrated both.

Decision 5: Acquire CaratLane

This may ultimately become one of the most important decisions in Titan’s history.

CaratLane provides:

- Younger customers

- Digital capabilities

- Omnichannel expertise

- Faster product cycles

Perhaps most importantly, it helps Titan remain relevant to future generations of jewellery buyers.

Decision 6: Acquire Damas Jewellery

The Damas acquisition is arguably Titan’s most ambitious strategic move.

For years, international expansion remained relatively modest.

Damas changes that.

The acquisition instantly strengthens Titan’s presence in the GCC region and accelerates its global ambitions.

The upside is significant.

So is the execution risk.

This will likely become one of the defining management tests of the next decade.

Capital Allocation Insight

Great management teams do not simply invest in today’s opportunities.

They invest in tomorrow’s opportunities before everyone else recognizes them.

Titan’s investments in CaratLane and international expansion fit this pattern.

What Earnings Calls Reveal About Management Quality

One of the most underrated sources of insight is management language.

Numbers tell you what happened.

Language often reveals how management thinks.

After reviewing multiple earnings calls, investor presentations, and annual reports, several patterns emerge.

Pattern 1: They Rarely Overpromise

Many management teams constantly talk about:

- Massive opportunities

- Transformational growth

- Industry disruption

- Market domination

Titan’s management generally avoids this style.

Their communication is typically operational.

They discuss:

- Store additions

- Buyer growth

- Product mix

- Gold-price impact

- Margin movement

- Consumer behavior

This may sound less exciting.

For investors, it is usually a positive sign.

Pattern 2: Problems Are Explained, Not Hidden

Several examples illustrate this.

During FY25, customs duty changes created inventory-related profitability pressure.

Management did not attempt to obscure the issue.

Instead, they:

- Quantified the impact

- Explained the mechanism

- Discussed expected timelines

- Reaffirmed long-term strategy

This improves credibility.

Investors can tolerate bad news.

What destroys trust is unclear communication.

Pattern 3: External Factors Are Acknowledged, Not Blamed

Across earnings calls, management referenced:

- Heatwaves

- Elections

- Gold prices

- Wedding-date variations

- Macroeconomic conditions

However, these references rarely became excuses.

Instead, management typically explained how the business adapted.

This distinction matters.

Strong management teams explain challenges.

Weak management teams explain away challenges.

Titan generally falls into the first category.

Pattern 4: Customer-Centric Thinking

One recurring theme across annual reports and earnings calls is customer focus.

Management frequently discusses:

- Buyer growth

- Consumer preferences

- Premiumization

- Exchange programs

- Design innovation

This may appear obvious.

It isn’t.

Many companies become obsessed with competitors.

Titan appears more focused on customers.

That mindset often creates better long-term outcomes.

The Leadership Transition Test

One of the most important developments for investors is the transition from:

C.K. Venkataraman

to

Ajoy Chawla

Leadership transitions create uncertainty.

Even successful companies can stumble during transitions.

The good news is that Titan’s transition appears planned rather than reactive.

Ajoy Chawla is not an outsider attempting to reinvent the company.

He is a long-time insider with deep operational understanding.

This reduces execution risk significantly.

However, investors should still monitor:

- Capital allocation discipline

- Growth priorities

- International strategy

- Damas integration

The true quality of leadership transitions becomes visible only after several years.

Areas Where Investors Should Remain Skeptical

Even high-quality management deserves scrutiny.

Several areas warrant ongoing monitoring.

International Expansion

International retail has historically been difficult for many Indian consumer companies.

Success in India does not automatically translate overseas.

The Damas acquisition increases opportunity.

It also increases complexity.

Emerging Businesses

Management continues investing in:

- Taneira

- Fragrances

- Women’s Bags

The strategy makes sense.

But investors should monitor whether these businesses eventually generate attractive returns.

Capital Allocation Discipline

As Titan grows larger, deploying capital efficiently becomes harder.

Management’s challenge is no longer finding growth opportunities. It is finding growth opportunities that meet Titan’s return standards.

Why This Matters

The larger a company becomes,

the harder it becomes to maintain high returns on capital.

Future management quality will be measured by capital allocation discipline more than revenue growth.

Forensic Assessment: What Does Management Behavior Suggest?

After reviewing:

- 10 years of annual reports

- Multiple investor presentations

- FY25 earnings calls

- FY26 earnings calls

- Quarterly commentary

- Strategic acquisitions

a consistent pattern emerges.

Management communication is generally:

Confident

Yes.

Promotional

Rarely.

Defensive

Only when addressing short-term profitability pressures.

Evasive

Very little evidence.

Transparent

Generally strong.

Execution-Oriented

Consistently.

Equity Blueprint Management Scorecard

| Parameter | Rating |

| Strategic Vision | 9/10 |

| Capital Allocation | 9/10 |

| Transparency | 9/10 |

| Shareholder Communication | 8.5/10 |

| Execution Track Record | 9.5/10 |

| Risk Management | 8.5/10 |

| Leadership Continuity | 8.5/10 |

Overall Management Quality Score

9/10

Layer 3 Verdict

Titan’s growth cannot be explained solely by favorable industry trends.

The evidence strongly suggests that management deserves substantial credit.

Over the last decade, leadership has:

- Built category-leading brands

- Expanded intelligently

- Managed crises effectively

- Maintained investor trust

- Allocated capital successfully

- Preserved high returns on capital

No management team is perfect.

Future challenges remain.

International expansion.

Damas integration.

Leadership transition.

Emerging-business profitability.

These will determine the next chapter.

But based on the evidence available today, Titan’s management ranks among the strongest leadership teams in Indian consumer retail.

That is a major reason the market continues assigning premium valuations to the business.

However, even great management teams cannot eliminate risk.

And every investment ultimately comes down to risk versus reward.

That brings us to Layer 4.

Layer 4: Risk Identification — What Could Actually Go Wrong for Titan?

One of the biggest mistakes investors make is assuming that a great business is automatically a low-risk investment.

History repeatedly proves otherwise.

Some of the largest wealth destroyers in stock market history were once considered unbeatable.

Nokia dominated mobile phones.

Kodak dominated photography.

General Electric was once viewed as the gold standard of corporate excellence.

Business quality and investment risk are not the same thing.

Titan is undoubtedly one of India’s strongest consumer franchises.

That does not mean investors should ignore risk.

In fact, premium businesses often require even more careful risk analysis because expectations are already extremely high.

The key is separating temporary volatility from permanent impairment.

Not all risks are equal.

Some create short-term noise.

Others can fundamentally alter the investment thesis.

Let’s examine both.

Understanding Titan’s Risk Framework

Titan faces two broad categories of risk:

1. Cyclical Risks

Temporary challenges that fluctuate with economic conditions.

Examples:

- Gold prices

- Consumer sentiment

- Economic slowdowns

- Interest rates

These typically affect short-term performance.

2. Structural Risks

Risks capable of altering long-term economics.

Examples:

- Competition

- Capital allocation mistakes

- Failed acquisitions

- Industry disruption

These matter far more.

Investors should spend less time worrying about quarterly volatility and more time evaluating structural threats.

Risk #1: Valuation Risk (The Biggest Risk Nobody Talks About)

Most investors immediately think of gold prices when discussing Titan.

Ironically, gold may not be the biggest risk at all.

Valuation probably is.

At roughly 70x earnings, Titan is priced for continued excellence.

The market is already assuming:

- Market-share gains continue

- Premiumization continues

- International expansion succeeds

- Margins remain healthy

- Returns on capital stay high

When expectations become elevated, even good outcomes can disappoint investors.

This is one of the most misunderstood concepts in investing.

Consider two scenarios.

Scenario A

Titan grows earnings 20% annually.

Valuation remains stable.

Shareholders do very well.

Scenario B

Titan grows earnings 20% annually.

Valuation compresses from 70x earnings to 45x earnings.

Business performance remains excellent.

Investor returns become dramatically lower.

This phenomenon has hurt investors in many premium businesses globally.

The business wins.

The stock underperforms.

The Most Important Risk

Titan’s biggest threat may not be operational failure.

It may simply be that investors have become too optimistic.

Risk #2: Gold Price Volatility

Gold remains the lifeblood of Titan’s jewellery business.

And gold prices have become increasingly volatile.

This creates both opportunities and challenges.

How Rising Gold Prices Help

Higher gold prices increase:

- Revenue realization

- Inventory values

- Consumer investment demand

During periods of uncertainty, gold often becomes more attractive as a store of value. This can support demand.

How Rising Gold Prices Hurt

At extremely high levels, gold becomes less affordable.

Consumers may:

- Postpone purchases

- Reduce purchase quantities

- Shift to lighter jewellery

- Delay discretionary spending

Management has repeatedly discussed these dynamics in earnings calls.

While demand has remained resilient, affordability pressures are real.

The Long-Term View

Historically, Indian consumers have shown remarkable resilience toward gold purchases.

The bigger risk is not demand destruction.

The bigger risk is temporary volume pressure and margin volatility.

Risk #3: Competitive Intensity Is Increasing

Titan remains the industry leader.

But leadership does not guarantee permanent dominance.

The jewellery industry is becoming increasingly competitive.

Several organized players are scaling aggressively.

Major Competitors

Kalyan Jewellers

Perhaps Titan’s most serious challenger.

Strong brand recognition.

Aggressive expansion.

Improving execution.

Senco Gold

Strong regional presence.

Rapid growth.

Competitive valuation.

Thangamayil Jewellery

Particularly strong in South India.

Deep local relationships.

Efficient operations.

Regional Jewellers

Thousands of local players continue competing on:

- Relationships

- Familiarity

- Convenience

- Local trust

Many are becoming more sophisticated.

Can Titan Lose Market Share?

Yes.

Absolutely.

No company gains market share forever.

The more realistic question is:

Can Titan continue growing despite increased competition?

The answer appears to be yes.

However, investors should expect market-share gains to become harder over time.

Competitive Reality

Titan does not need competitors to fail.

Titan simply needs to grow faster than them.

That is a much more achievable objective.

Risk #4: International Expansion Risk

International growth is one of Titan’s most exciting opportunities.

It is also one of its most uncertain.

History provides many examples of successful domestic businesses struggling overseas.

Consumer behavior changes.

Brand recognition changes.

Competitive landscapes change.

Regulatory frameworks change.

Success is never guaranteed.

The Damas Acquisition Test

The acquisition of Damas Jewellery represents a major strategic milestone.

Potential upside:

✔ Accelerated GCC expansion

✔ Larger customer base

✔ Greater global relevance

✔ Stronger international distribution

Potential downside:

✖ Integration complexity

✖ Cultural challenges

✖ Margin pressure

✖ Execution risk

The acquisition is not automatically good or bad.

Its success will depend entirely on execution.

Investors should closely monitor:

- Profitability

- Store productivity

- Brand positioning

- Integration progress

Over the next three years.

Risk #5: Working Capital Intensity

Many investors underestimate this risk.

Jewellery retail requires massive inventory.

Gold must be:

- Purchased

- Stored

- Secured

- Financed

- Managed

This creates substantial working-capital requirements.

Titan’s inventory levels naturally increase as:

- Gold prices rise

- Store count expands

- Product variety expands

This ties up capital.

Why It Matters

Working-capital-heavy businesses often struggle to convert accounting profits into cash.

Fortunately, Titan has historically managed inventory efficiently.

But investors should continue monitoring:

- Inventory turnover

- Cash flow conversion

- Financing costs

Especially during periods of rapid growth.

Risk #6: Leadership Transition Risk

Every leadership transition introduces uncertainty.

The transition from C.K. Venkataraman to Ajoy Chawla appears smooth.

However, investors should remember:

Strong institutions outlast individual leaders.

But leadership still matters.

Future strategic decisions will determine:

- Capital allocation

- International expansion

- M&A activity

- Growth priorities

The transition appears well-managed today.

The true assessment will emerge over several years.

Risk #7: Emerging Businesses May Never Scale

Titan continues investing in:

- Taneira

- SKINN

- Women’s Bags

- Other emerging categories

The strategy is logical.

Build future growth engines before they are needed.

But investors should recognize a simple reality.

Not every initiative succeeds.

Some businesses may:

- Grow slower than expected

- Remain unprofitable longer

- Fail to achieve scale

The good news is that jewellery generates sufficient cash flow to absorb these experiments.

The risk is manageable.

But it should not be ignored.

Risk #8: Regulatory Risk

The jewellery industry remains heavily influenced by policy.

Potential regulatory changes include:

- Import duties

- Hallmarking requirements

- Taxation changes

- Gold financing regulations

The FY25 customs-duty impact demonstrated how policy changes can affect profitability even when the long-term outcome is positive. Investors should expect regulatory volatility to remain part of the industry.

Probability-Weighted Risk Assessment

Probability-Weighted Risk Assessment

| Risk | Probability | Impact | Overall Importance |

| Valuation Compression | High | High | Very High |

| Gold Price Volatility | High | Medium | High |

| Competition | Medium | Medium | Medium |

| Damas Integration | Medium | High | High |

| Working Capital Pressure | Medium | Medium | Medium |

| Leadership Transition | Low-Medium | Medium | Medium |

| Emerging Business Failures | Medium | Low | Low |

| Regulatory Changes | Medium | Medium | Medium |

What Is NOT a Major Risk?

Interestingly, several commonly cited risks appear less concerning.

Demand for Gold Disappearing

Unlikely.

Gold remains deeply embedded in Indian culture.

Brand Relevance

Low risk.

Titan continues investing heavily in design, marketing, and customer engagement.

Financial Distress

Very low risk.

The balance sheet remains healthy.

Returns on capital remain strong.

Corporate Governance

No major red flags identified through annual reports, earnings calls, or capital allocation behavior.

Risk Summary

Titan’s greatest risks are not existential.

They are expectations risks.

The company is unlikely to fail.

The bigger question is whether future performance can remain strong enough to justify the market’s optimism.

Equity Blueprint Assessment: Layer 4

Major Strengths

✔ Industry leadership

✔ Trusted brands

✔ Strong balance sheet quality

✔ High return on capital

✔ Long growth runway ✔ Strong management credibility

Major Risks

✖ Premium valuation

✖ Gold-price volatility

✖ International execution

✖ Competitive intensity

✖ Working-capital requirements

Layer 4 Verdict

Titan faces risks.

Every investment does.

However, most of Titan’s risks are execution and valuation risks rather than survival risks.

That distinction is critical.

The probability of Titan becoming a materially weaker business appears relatively low.

The probability of investor returns being affected by valuation compression is considerably higher.

This makes Titan a fascinating case study.

The business appears safer than the stock.

The final question therefore becomes:

Does the quality of the business justify the valuation investors are being asked to pay?

That is what we will answer in Layer 5.

Layer 5: Decision Discipline — Does Titan Deserve Your Capital Today?

Investing is often portrayed as a search for great companies.

In reality, investing is a search for attractive risk-adjusted returns.

Those two objectives are not always the same.

A mediocre company purchased at an exceptionally low valuation can sometimes outperform a great company purchased at an excessively high valuation.

That is why the final step of the Equity Blueprint framework is not asking:

“Is Titan a great business?”

We already know the answer.

The more important question is:

“Does Titan deserve fresh capital allocation today?”

To answer that question, investors must combine everything discussed so far.

Not just valuation.

Not just growth.

Not just management.

All five layers together.

Only then does a complete picture emerge.

The Titan Investment Checklist

Let’s evaluate Titan through the Equity Blueprint lens.

Layer 1: Valuation Discipline

Assessment

Mixed.

Titan is unquestionably expensive relative to peers.

However, it is not unusually expensive relative to its own history.

The market continues assigning premium multiples because Titan continues delivering premium execution.

The challenge is that future returns are increasingly dependent on earnings growth rather than valuation expansion.

Verdict

Passes, but with caution.

Layer 2: Growth Consistency

Assessment

Exceptional.

Revenue increased from approximately ₹11,913 crore to ₹87,584 crore over the last decade.

Profit increased from approximately ₹1,153 crore to ₹8,355 crore.

Most importantly, growth survived:

- Demonetization

- GST

- COVID

- Gold-price volatility

- Regulatory changes

This suggests structural rather than cyclical growth.

Verdict

Strong Pass.

Layer 3: Management Execution

Assessment

Excellent.

Management has consistently demonstrated:

- Rational capital allocation

- Strong communication

- Disciplined expansion

- Long-term thinking

There is little evidence of promotional behavior or narrative inflation.

Verdict

Strong Pass.

Layer 4: Risk Identification

Assessment

Manageable.

The primary risks are:

- Valuation compression

- Gold-price volatility

- International execution

- Competitive intensity

Importantly, most risks appear operational rather than existential.

Verdict

Passes.

The Most Important Insight From This Entire Analysis

Titan’s biggest challenge is no longer proving that it is a great company.

The market already believes that.

Titan’s challenge is proving that it can remain exceptional for long enough to justify an exceptional valuation.

This distinction matters enormously.

Many investors spend their energy trying to identify good businesses.

The harder task is identifying good businesses that are still capable of outperforming expectations.

Titan has already exceeded expectations for decades.

Future success becomes progressively harder because expectations continue rising.

The Equity Blueprint Principle

The quality of a business determines whether it deserves your attention.

The valuation determines whether it deserves your capital.

Titan easily wins the first test. The second test is more complicated.

What Must Go Right For Titan?

For Titan to continue compounding shareholder wealth at attractive rates, several things need to happen.

1. Organized Market Share Must Continue Rising

The migration from unorganized to organized jewellery retail remains the largest long-term opportunity.

Titan does not need to dominate the entire market.

It simply needs to continue capturing a meaningful share of this migration.

2. Premiumization Must Continue

Consumers must continue moving toward:

- Branded jewellery

- Better designs

- Higher-ticket purchases

- Trusted retailers

Titan’s economics improve significantly when premiumization continues.

3. Damas Integration Must Succeed

The Damas acquisition has the potential to become a major value creator.

Successful integration could significantly strengthen Titan’s international business.

Poor execution could dilute returns.

4. CaratLane Must Continue Scaling

CaratLane is increasingly important because it connects Titan with younger consumers.

Continued expansion and profitability improvements would strengthen the long-term investment thesis.

5. Returns on Capital Must Remain High

One of Titan’s greatest strengths has been its ability to generate exceptional returns despite inventory intensity. Maintaining those returns will be critical.

What Could Break The Thesis?

Investors should also understand what could weaken the investment case.

Warning Sign #1

Sustained market-share losses.

Warning Sign #2

Material deterioration in ROE and ROCE.

Warning Sign #3

Weak execution in international markets.

Warning Sign #4

Persistent margin pressure.

Warning Sign #5

Aggressive acquisitions that dilute capital allocation discipline.

Warning Sign #6

Rapid deterioration in cash-flow conversion.

Titan’s Place in a Long-Term Portfolio

Not every stock serves the same purpose.

Some stocks are:

- Deep value opportunities

- Turnaround candidates

- Cyclical bets

- Speculative growth stories

Titan belongs to a different category.

Titan is a compounder.

Compounders rarely look cheap.

They create wealth by:

- Growing steadily

- Reinvesting intelligently

- Compounding earnings over long periods

The challenge is that investors often underestimate how much future growth is already reflected in the stock price. That makes entry discipline important.

Equity Blueprint Scorecard

| Category | Score |

| Industry Quality | 9.5/10 |

| Competitive Position | 9.5/10 |

| Growth Visibility | 9/10 |

| Management Quality | 9/10 |

| Balance Sheet Quality | 8/10 |

| Capital Allocation | 9/10 |

| Risk Profile | 8/10 |

| Valuation Comfort | 5.5/10 |

Overall Equity Blueprint Rating

8.5 / 10

Final Verdict

🏆 Equity Blueprint Classification

STRUCTURAL BUY

With One Important Caveat:

It is a premium business at a premium price.

Titan possesses nearly every characteristic long-term investors seek:

✔ Industry leadership

✔ Powerful brands

✔ High returns on capital

✔ Strong management

✔ Long growth runway

✔ Multiple future growth engines

✔ Structural industry tailwinds

However, investors should recognize that future returns are likely to be driven by earnings growth rather than valuation expansion.

The margin of safety is not particularly large.

This is not a bargain purchase.

This is a quality purchase.

For investors with a long investment horizon and realistic return expectations, Titan remains one of India’s strongest consumer franchises.

For investors seeking deep value, better opportunities may exist elsewhere.

Final Takeaway

Titan transformed trust into a business model.

Then it transformed that business model into one of India’s greatest consumer franchises.

The question is no longer whether Titan is a great company.

The question is whether it can remain great enough for long enough to justify one of the market’s richest valuations.

Key Metrics To Monitor Every Quarter

Investors should track:

Jewellery Segment Growth

The core engine of the business.

Same Store Sales Growth (SSSG)

Indicates underlying demand strength.

Market Share Gains

Measures formalization benefits.

CaratLane Growth

Important indicator of future customer acquisition.

International Revenue

Critical for the next growth phase.

Damas Integration Progress

One of management’s biggest strategic tests.

ROE & ROCE

Measures capital allocation efficiency.

Operating Cash Flow

Confirms earnings quality.

Inventory Growth

Tracks working-capital discipline.

Margin Trends

Provides early warning of competitive pressure.

Frequently Asked Questions (FAQ)

Is Titan stock overvalued at 70x P/E?

Titan is expensive relative to peers but not unusually expensive relative to its own history. Investors are paying for business quality, market leadership, and long-term growth visibility. The primary risk is valuation compression rather than business deterioration.

Is Titan better than Kalyan Jewellers?

Titan currently enjoys stronger brand equity, higher profitability, superior returns on capital, and broader diversification. Kalyan, however, trades at a significantly lower valuation and may offer higher growth potential from a smaller base.

Why does Titan trade at such a high valuation?

The market views Titan as a consumer franchise rather than a traditional jewellery retailer. Investors are paying for trust, market leadership, premium brands, capital efficiency, and a long growth runway.

Can Titan become a ₹10 lakh crore company?

Mathematically, yes. Achieving that milestone would likely require continued industry formalization, successful international expansion, sustained premiumization, and strong capital allocation over many years.

What happens if gold prices keep rising?

Higher gold prices can support revenue growth but may temporarily affect affordability and volume growth. Historically, Indian consumers have remained resilient buyers of gold, particularly during weddings and festivals.

Is Titan a good stock for long-term wealth creation?

Titan possesses many characteristics associated with long-term compounders, including strong competitive advantages, high returns on capital, credible management, and structural growth drivers. However, valuation remains a critical consideration for new investors.

What is the biggest risk for Titan investors?

The biggest risk today is valuation risk. The business may continue performing well while stock returns disappoint if valuation multiples decline.

Is Titan still primarily a jewellery company?

Yes. Jewellery remains the dominant revenue and profit contributor. However, watches, CaratLane, EyeCare, fragrances, and international operations are becoming increasingly important to the broader growth story.

Data Sources & Attribution:

Market Data: Real-time price action and corporate announcements provided via the National Stock Exchange of India (NSE) https://www.nseindia.com/

Financial Metrics: Historical fundamental data, ratios, and peer comparisons sourced from Screener.in https://www.screener.in/

Company Disclosures: Statutory filings, annual reports, and investor presentations sourced directly from the Company’s Investor Relations desk. https://www.titancompany.in/

Related Analysis:

Rajesh Exports: Revenue Up 15x, Profit Down 91% — What Are The Numbers Trying To Tell Investors? Rajesh Exports: Revenue Up 15x, Profit Down 91% — What Are The Numbers Trying To Tell Investors?

Disclaimer

The analysis provided on this blog, including the “5-Layer Framework,” is for educational and informational purposes only. I am not a SEBI-registered investment advisor. Stock market investing involves significant risk, and past performance is not indicative of future results. The views expressed here are my personal opinions based on my research and study of financial literature. This is not a buy or sell recommendation. Please conduct your own due diligence or consult a qualified, SEBI-registered financial advisor before making any investment decisions. The author may or may not hold positions in the stocks discussed.

About the Author

Nilendu Chatterjee is the founder of Equity Blueprint, a platform focused on helping retail investors approach the stock market with clarity, structure, and discipline. With over a decade of experience in the industrial sector and a strong passion for equity research, he brings a practical, ground-level perspective to fundamental analysis.

Through a framework-driven approach, Nilendu breaks down complex businesses into simple, decision-oriented insights—bridging the gap between professional-grade research and everyday investing. His work is centered on one goal: enabling long-term wealth creation by replacing speculation with structured thinking.